One big reason we’re not facing a foreclosure crisis right now is the significant amount of equity that homeowners have. Unlike during the last housing bubble, when many homeowners found themselves owing more than their homes were worth, today’s homeowners have a lot more equity compared to their debt.

Mortgage debt is at an all-time high, but that’s a big reason why we’re not experiencing a repeat of 2008. Bill McBride, a housing analyst for Calculated Risk, points out that this situation is different.

““With the recent house price increases, some people are worried about a new housing bubble – but mortgage debt isn’t a concern . . .”

”

Today’s homeowners find themselves in a much more advantageous situation than ever. Let’s take a closer look and understand why today’s mortgage debt isn’t something to worry about.

More Equity, Less Risk of Foreclosures

The St. Louis Fed reports that homeowner equity is now almost three times greater than the total mortgage debt.

Having high equity in a home reduces the chances of foreclosure since homeowners have more alternatives. If someone finds it difficult to keep up with their mortgage payments, they could consider selling their house. This way, they might still make a profit because of the equity they’ve accumulated.

Even if home values drop, many homeowners would still have a good amount of equity to fall back on. This is quite different from the 2008 crisis, when a lot of homeowners owed more on their mortgages than their homes were worth and faced limited choices to prevent foreclosure.

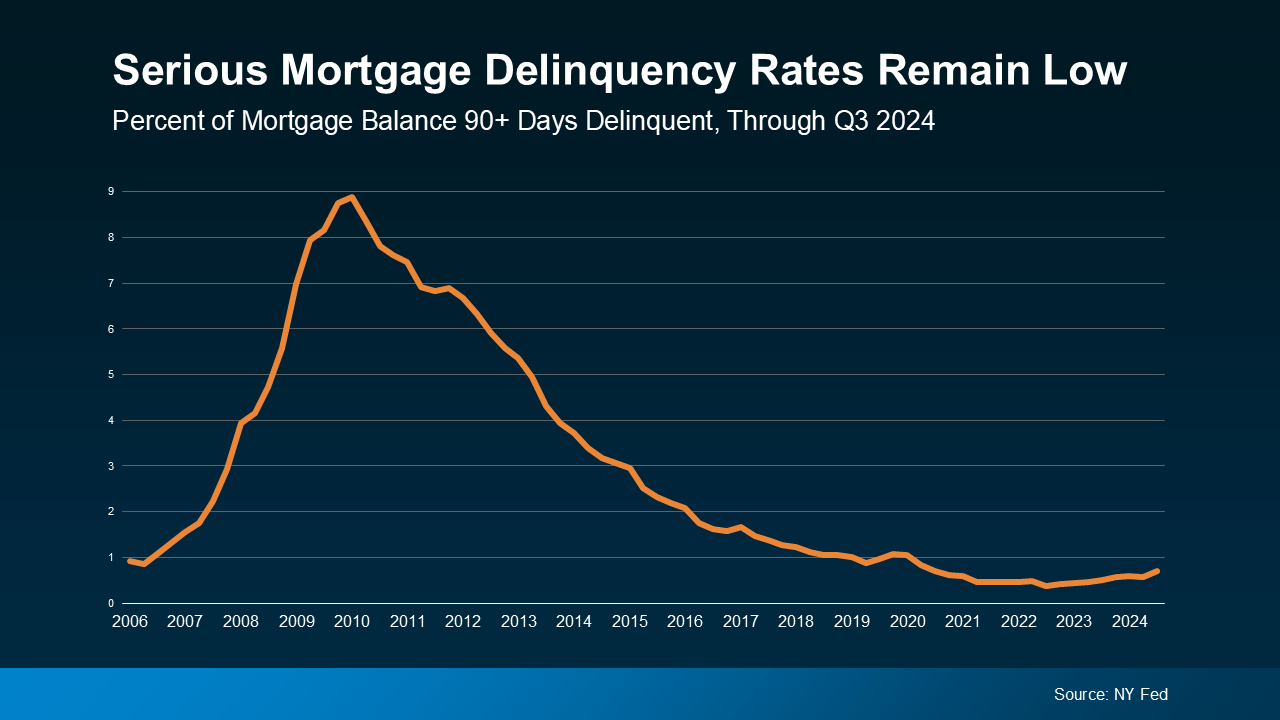

Delinquency Rates Are Still Near Historic Lows

Another encouraging sign is that, based on data from the NY Fed, the number of mortgage payments that are over 90 days late remains close to historic lows.

This is partly because of several programs aimed at assisting homeowners facing temporary challenges. As Marina Walsh, VP of Industry Analysis at the Mortgage Bankers Association (MBA), points out:

““. . . servicers are helping at-risk homeowners avoid foreclosures through loan workout options that can mitigate temporary distress.”

”

Even if someone is struggling with their payments, there are resources available to help them steer clear of foreclosure.

Low Unemployment Helps Keep the Market Stable

Today's low unemployment rate is another key factor to consider. Since more people have stable jobs, they're in a better position to afford their mortgage payments. As Archana Pradhan, Principal Economist at CoreLogic, points out:

““Low unemployment numbers have helped reduce the overall delinquency rate . . .”

”

During the last housing crisis, there was a significant rise in unemployment, which resulted in many foreclosures. However, the current unemployment rate looks quite different.

That consistent employment level is one reason the market lacks the same risks it faced last time.

You don’t need to be concerned about a surge in distressed sales similar to what happened in 2008. Nowadays, most homeowners are employed and have manageable low-interest mortgages that they can comfortably pay. As McBride noted, this stability plays a key role in the current market.

““The bottom line is there will not be a huge wave of distressed sales as happened following the housing bubble.”

”

Bottom Line

While mortgage debt levels are elevated, there’s no need to worry about the market facing another crash. In fact, many homeowners are in a solid position. If you have any questions or concerns, let’s talk.